The Village Global podcast takes you inside the world of venture capital and technology, featuring enlightening interviews with entrepreneurs, investors and tech industry leaders. Learn more at www.villageglobal.vc.

…

continue reading

Content provided by Stuart Wemyss. All podcast content including episodes, graphics, and podcast descriptions are uploaded and provided directly by Stuart Wemyss or their podcast platform partner. If you believe someone is using your copyrighted work without your permission, you can follow the process outlined here https://player.fm/legal.

Similar to Investopoly

An archive of each full weekday episode of the award-winning program presented by Bruce Whitfield.

…

continue reading

Bitcoin groundbreakers share personal stories of how Bitcoin is changing lives for the better. Host Mauricio Di Bartolomeo, co-founder and CSO of Ledn, speaks with leading Bitcoin voices, entrepreneurs, and human rights advocates to hear their unique journey and practical real-world examples of how Bitcoin has made a positive impact in their lives. Brought to you by Ledn, a leading financial services company built for Bitcoin & digital assets. Ledn offers a suite of lending, saving and tradi ...

…

continue reading

Bitcoin pioneer Charlie Shrem peels back the layers on the lives and backgrounds of the world's most impactful innovators. Centering around intimate narratives, Shrem uncovers a detailed, previously unspoken story of the genesis and evolution of bitcoin, cryptocurrency, artificial intelligence, and the web3 movements. Join Shrem as he journeys through the uncharted territories of tech revolutions, revealing the human side of the stories that shaped the digital world we live in today.

…

continue reading

How will countries around the world cope with persistent inflation and high borrowing costs? Are central bankers helping to abate the cost-of-living crisis or are they moving us all closer to recession? On Stephanomics, a podcast hosted by Bloomberg Economics head Stephanie Flanders—the former BBC economics editor and chief market strategist for Europe at JPMorgan Asset Management—we combine reports from Bloomberg journalists around the world and conversations with internationally respected ...

…

continue reading

Bloomberg Radio host Barry Ritholtz looks at the people and ideas that shape markets, investing and business.

…

continue reading

Best friends Joel and Matt are the co-hosts of How to Money which is all about providing the knowledge & tools that normal folks need to thrive in areas like debt payoff, DIY investing, and crucial money tricks that will provide continuous help along your journey. We believe that access to unbiased and jargon-free personal finance guidance is more necessary than ever before. When you handle your money in a purposeful, thoughtful way that works for your lifestyle, you can really start living ...

…

continue reading

Ever wondered what makes great go-to-market leaders grow, even when the going gets tough? We have, too. And we’re on a mission to uncover the magic that makes that growth happen. This is Go-to-Market Magic, the show where we talk to go-to-market leaders and visionaries about the “aha!” moments they experience and the pivotal decisions they’ve made, all in the name of growth. And we’re not just talking about revenue growth that goes up and to the right — we’ll also discuss how they improve th ...

…

continue reading

The Partnership Economy explores the power of partnerships through candid conversations and stories with industry leaders. Our hosts, David A. Yovanno, CEO and Todd Crawford, Co-founder, of impact.com, unpack the future of partnerships as a lever for scale and an opportunity to put the consumer first.

…

continue reading

A weekly roundup of the most important stories from the worlds of business and finance, hosted by Felix Salmon.

…

continue reading

Player FM - Podcast App

Go offline with the Player FM app!

Go offline with the Player FM app!

))

Where are interest rates heading and what should you do?

Manage episode 229676928 series 2094305

Content provided by Stuart Wemyss. All podcast content including episodes, graphics, and podcast descriptions are uploaded and provided directly by Stuart Wemyss or their podcast platform partner. If you believe someone is using your copyrighted work without your permission, you can follow the process outlined here https://player.fm/legal.

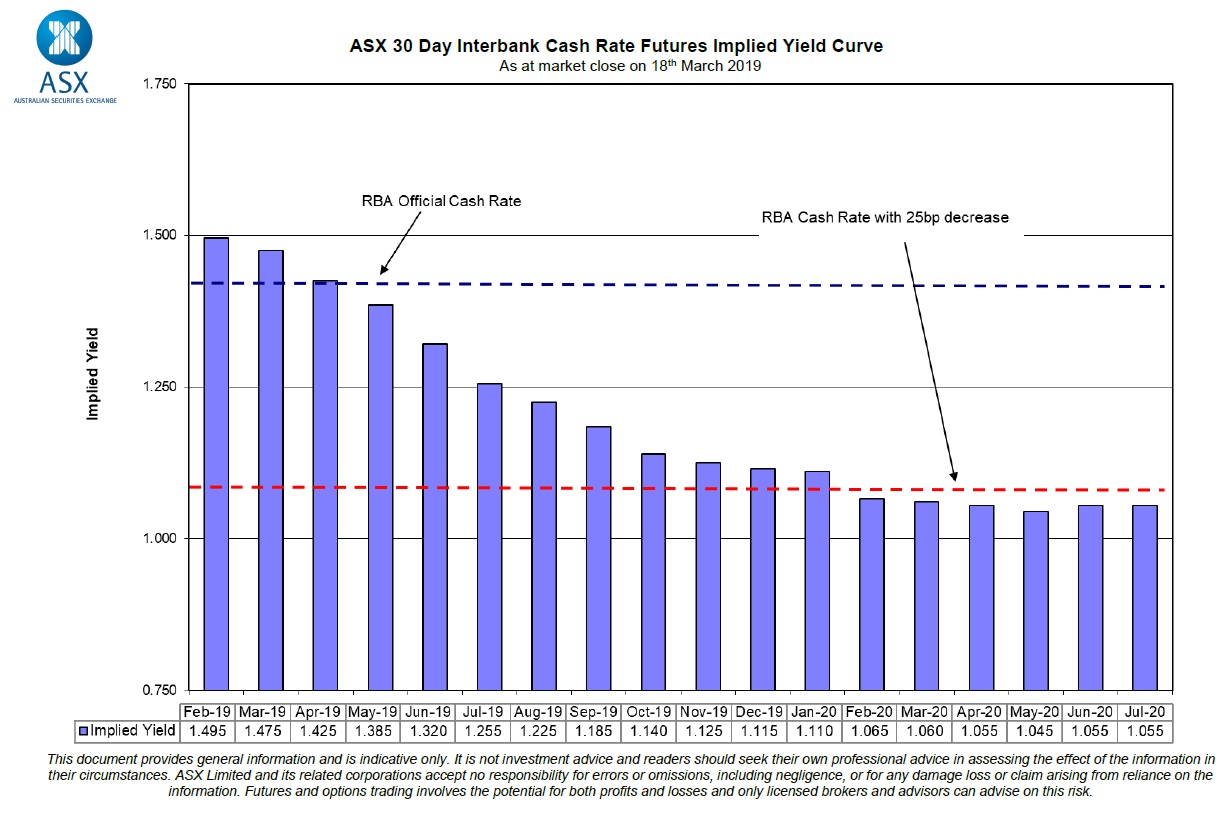

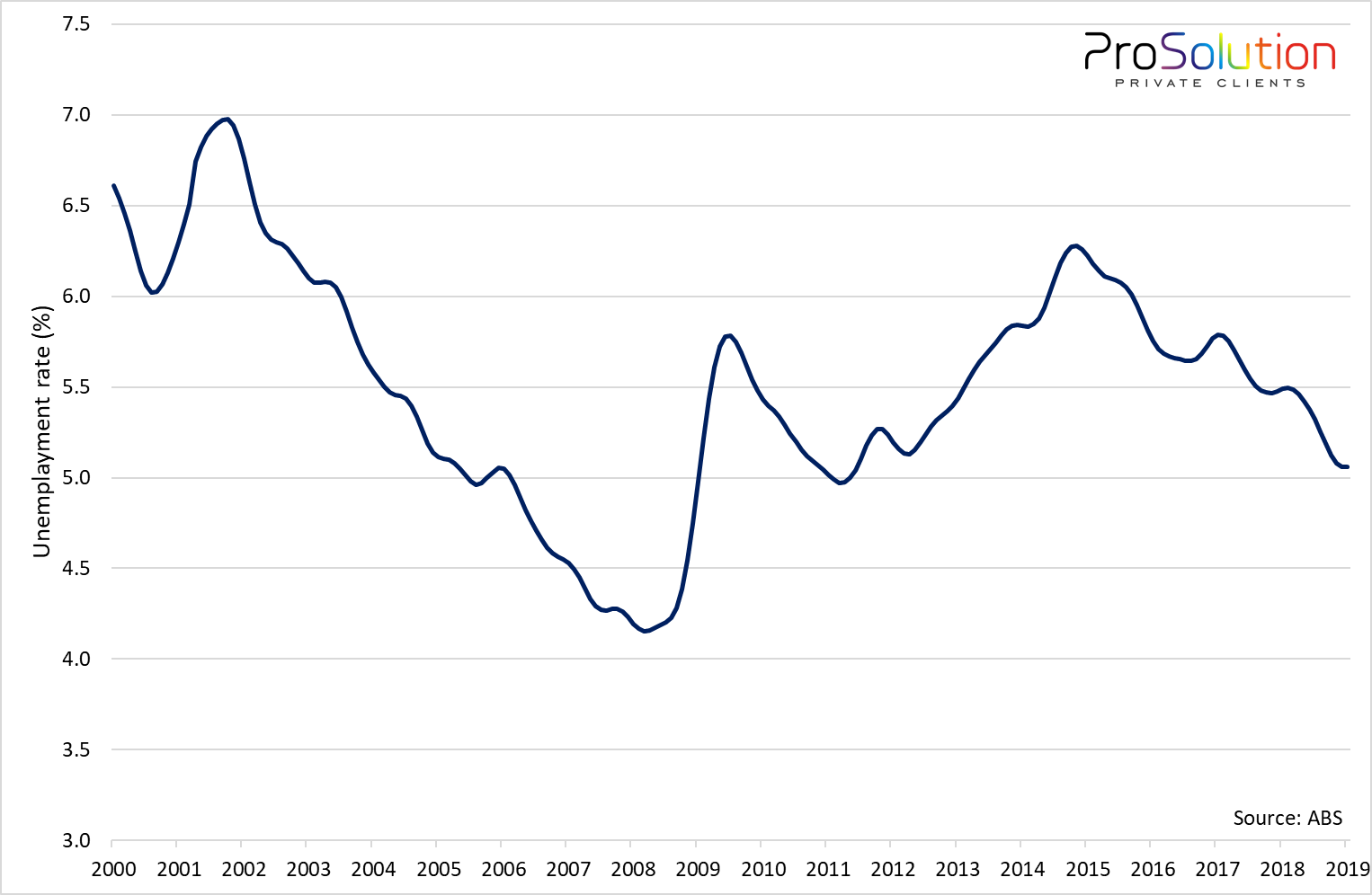

For many Australian's, their home loan is their largest expense. And property investors should seek to minimise their borrowing costs (interest) as it's one of the top three factors that directly impacts investment success as outlined in this blog. With this in mind, I thought it was timely to look at the current opportunities in the mortgage/interest rate market. What the "market" is expecting As the chart below illustrates, the implied yield on 30-day cash rate futures suggests that the market expects the cash rate to be 0.25% lower in the second half of 2019. These future contracts are used primarily by large institutions and banks and essentially represent the consensus view on the direction of interest rates in the short term (i.e. next 18 months). Of course, the market is not always right - it's only one indicator. https://www.prosolution.com.au/wp-content/uploads/2019/03/cash-rate-futuresv2.jpg Economist predictions Bill Evans, the Chief Economist for Westpac, was the first to predict that the RBA will cut its cash rate twice in 2019 (0.25% in August and then again in November). Since making this prediction on 20 February 2019, many other economists have joined him. Mr Evans was the first economist to correctly predict the start of the RBA's easing cycle in 2011 - so he has good form. Mr Evans cited weaker than expected GDP growth, the "wealth effect"[1] associated with a softer property market and an expected increase in our savings rate as the main reasons for forming his view. What would have to happen for the RBA to cut The RBA has previously said on a number of occasions that it is not concerned by the falling house prices. This commentary has never made sense to me because a falling property market definitely impacts on consumer confidence - look at what happened in the USA when the GCF hit. Perhaps the RBA was hoping its positive rhetoric would persuade Australian's to ignore the wealth effect. However, in the last few weeks the RBA has changed its tune and acknowledge the risk that a soft property market might have on the wider economy. Also, the RBA has downgraded its GDP growth forecast. I think the RBA would need to see an increase in the unemployment rate before it would be willing to cut the cash rate. Australia's unemployment rate is still relatively low at 5.1% as illustrated in the chart below. https://www.prosolution.com.au/wp-content/uploads/2019/03/unemployment-rate.png Will the banks pass it on? Of course, if the RBA does cut the cash rate below its current level of 1.5% p.a., the big question is; will the banks pass all of the reduction onto borrowers? On one hand, given the scrutiny and negative publicity generated by the recent Royal Commission, you would think they would have to be very brave (read stupid or arrogant) to not pass it all on. That said, a few small lenders have increased variable rates this year (e.g. ING) which suggest funding costs have been on the rise. Perhaps the banks will use this opportunity to improve their...

…

continue reading

220 episodes

Manage episode 229676928 series 2094305

Content provided by Stuart Wemyss. All podcast content including episodes, graphics, and podcast descriptions are uploaded and provided directly by Stuart Wemyss or their podcast platform partner. If you believe someone is using your copyrighted work without your permission, you can follow the process outlined here https://player.fm/legal.

For many Australian's, their home loan is their largest expense. And property investors should seek to minimise their borrowing costs (interest) as it's one of the top three factors that directly impacts investment success as outlined in this blog. With this in mind, I thought it was timely to look at the current opportunities in the mortgage/interest rate market. What the "market" is expecting As the chart below illustrates, the implied yield on 30-day cash rate futures suggests that the market expects the cash rate to be 0.25% lower in the second half of 2019. These future contracts are used primarily by large institutions and banks and essentially represent the consensus view on the direction of interest rates in the short term (i.e. next 18 months). Of course, the market is not always right - it's only one indicator. https://www.prosolution.com.au/wp-content/uploads/2019/03/cash-rate-futuresv2.jpg Economist predictions Bill Evans, the Chief Economist for Westpac, was the first to predict that the RBA will cut its cash rate twice in 2019 (0.25% in August and then again in November). Since making this prediction on 20 February 2019, many other economists have joined him. Mr Evans was the first economist to correctly predict the start of the RBA's easing cycle in 2011 - so he has good form. Mr Evans cited weaker than expected GDP growth, the "wealth effect"[1] associated with a softer property market and an expected increase in our savings rate as the main reasons for forming his view. What would have to happen for the RBA to cut The RBA has previously said on a number of occasions that it is not concerned by the falling house prices. This commentary has never made sense to me because a falling property market definitely impacts on consumer confidence - look at what happened in the USA when the GCF hit. Perhaps the RBA was hoping its positive rhetoric would persuade Australian's to ignore the wealth effect. However, in the last few weeks the RBA has changed its tune and acknowledge the risk that a soft property market might have on the wider economy. Also, the RBA has downgraded its GDP growth forecast. I think the RBA would need to see an increase in the unemployment rate before it would be willing to cut the cash rate. Australia's unemployment rate is still relatively low at 5.1% as illustrated in the chart below. https://www.prosolution.com.au/wp-content/uploads/2019/03/unemployment-rate.png Will the banks pass it on? Of course, if the RBA does cut the cash rate below its current level of 1.5% p.a., the big question is; will the banks pass all of the reduction onto borrowers? On one hand, given the scrutiny and negative publicity generated by the recent Royal Commission, you would think they would have to be very brave (read stupid or arrogant) to not pass it all on. That said, a few small lenders have increased variable rates this year (e.g. ING) which suggest funding costs have been on the rise. Perhaps the banks will use this opportunity to improve their...

…

continue reading

220 episodes

All episodes

×Welcome to Player FM!

Player FM is scanning the web for high-quality podcasts for you to enjoy right now. It's the best podcast app and works on Android, iPhone, and the web. Signup to sync subscriptions across devices.

Similar to Investopoly

The Village Global podcast takes you inside the world of venture capital and technology, featuring enlightening interviews with entrepreneurs, investors and tech industry leaders. Learn more at www.villageglobal.vc.

…

continue reading

An archive of each full weekday episode of the award-winning program presented by Bruce Whitfield.

…

continue reading

Bitcoin groundbreakers share personal stories of how Bitcoin is changing lives for the better. Host Mauricio Di Bartolomeo, co-founder and CSO of Ledn, speaks with leading Bitcoin voices, entrepreneurs, and human rights advocates to hear their unique journey and practical real-world examples of how Bitcoin has made a positive impact in their lives. Brought to you by Ledn, a leading financial services company built for Bitcoin & digital assets. Ledn offers a suite of lending, saving and tradi ...

…

continue reading

Bitcoin pioneer Charlie Shrem peels back the layers on the lives and backgrounds of the world's most impactful innovators. Centering around intimate narratives, Shrem uncovers a detailed, previously unspoken story of the genesis and evolution of bitcoin, cryptocurrency, artificial intelligence, and the web3 movements. Join Shrem as he journeys through the uncharted territories of tech revolutions, revealing the human side of the stories that shaped the digital world we live in today.

…

continue reading

How will countries around the world cope with persistent inflation and high borrowing costs? Are central bankers helping to abate the cost-of-living crisis or are they moving us all closer to recession? On Stephanomics, a podcast hosted by Bloomberg Economics head Stephanie Flanders—the former BBC economics editor and chief market strategist for Europe at JPMorgan Asset Management—we combine reports from Bloomberg journalists around the world and conversations with internationally respected ...

…

continue reading

Bloomberg Radio host Barry Ritholtz looks at the people and ideas that shape markets, investing and business.

…

continue reading

Best friends Joel and Matt are the co-hosts of How to Money which is all about providing the knowledge & tools that normal folks need to thrive in areas like debt payoff, DIY investing, and crucial money tricks that will provide continuous help along your journey. We believe that access to unbiased and jargon-free personal finance guidance is more necessary than ever before. When you handle your money in a purposeful, thoughtful way that works for your lifestyle, you can really start living ...

…

continue reading

Ever wondered what makes great go-to-market leaders grow, even when the going gets tough? We have, too. And we’re on a mission to uncover the magic that makes that growth happen. This is Go-to-Market Magic, the show where we talk to go-to-market leaders and visionaries about the “aha!” moments they experience and the pivotal decisions they’ve made, all in the name of growth. And we’re not just talking about revenue growth that goes up and to the right — we’ll also discuss how they improve th ...

…

continue reading

The Partnership Economy explores the power of partnerships through candid conversations and stories with industry leaders. Our hosts, David A. Yovanno, CEO and Todd Crawford, Co-founder, of impact.com, unpack the future of partnerships as a lever for scale and an opportunity to put the consumer first.

…

continue reading

A weekly roundup of the most important stories from the worlds of business and finance, hosted by Felix Salmon.

…

continue reading

Player FM - Podcast App

Go offline with the Player FM app!

Go offline with the Player FM app!

{kind=link}

{kind=link}