))

Five Questions: Debt, Real Estate Investing and Freelancing

Archived series ("Inactive feed" status)

When?

This feed was archived on October 27, 2018 21:39 (

Why? Inactive feed status. Our servers were unable to retrieve a valid podcast feed for a sustained period.

What now? You might be able to find a more up-to-date version using the search function. This series will no longer be checked for updates. If you believe this to be in error, please check if the publisher's feed link below is valid and contact support to request the feed be restored or if you have any other concerns about this.

Manage episode 170738330 series 1344369

Content provided by Listen Money Matters. All podcast content including episodes, graphics, and podcast descriptions are uploaded and provided directly by Listen Money Matters or their podcast platform partner. If you believe someone is using your copyrighted work without your permission, you can follow the process outlined here https://player.fm/legal.

This week the guys tackle five questions from the audience on debt, real estate investing and freelancing.

Question one:

Hi, Andrew, Tom, and Laura, I think an important, and sorely needed topic is finance for freelancers. And not even those who use invoicing systems. I've been freelancing for more years than I care to admit, and there are so many like me who copyedit, proofread or design book jackets. We're one-person shows, with little-to-no cushion, where times are feast or famine. I would love to talk about this more or hear you guys talk about it in more depth. Putting together a financial system when you have variable income is uses the same fundamentals as someone who is a salaried employee. However, you'll have to build a bigger cushion if your income isn't consistent. You need to keep more in a reserve account than someone who has steady pay. Keep track of your income month to month and use that data to plan for the upcoming year. If you have a pool business and make most of your money from April to September, budget accordingly. Make sure you aren't overspending that income has to last you. Six months worth of expenses should be a big enough war chest to get you through a hard time if need be. If you are a freelancer and haven't earned in 6 months, maybe it's time to look into another career or pivot your business.Question Two:

Hey guys, Is it possible to rollover my Roth IRA to a traditional? Would I get a tax refund for the income tax that I would have saved had I been using a traditional IRA all along? Are there any limitations or conditions to performing this rollover? I have only had a Roth IRA for two years. There are some advantages of rolling over your Roth into a Traditional. If you're broke and need cash or you are retiring soon and aren't planning on earning in the future could be a reason to make this play. When you move money from a Roth retirement account to a traditional IRA, you can get back the taxes you paid on that contribution, but there are rules and deadlines. Be aware of the calendar deadlines that the IRS imposes.Question Three:

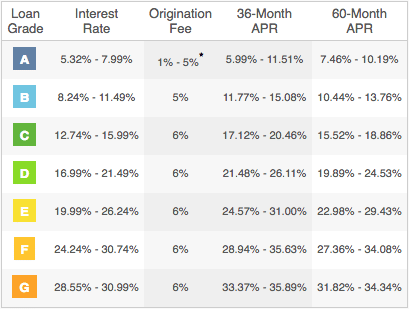

Hey guys, I am trying to refinance my credit card debt. I asked Lending Club for a $3,000 loan, and they are only giving me the option to take out a $6,025 loan. Do you know why this is? If this is my only option, I plan on taking it out and then giving back $3,025 right away since I only need 3k. What would you guys do? Is that even possible for me to give back $3,025 right away? Lending Club is a peer to peer lending service. That means, instead of going to a bank for a loan, you can get a loan from a group of random people. On the flip side of things, you can also contribute to funding a loan for other people allowing you to get in on the bank’s profit engine. Lending Club because they get better rates than they would with a bank loan and loans are issued much faster through the power of the crowd. The crowd will also approve loans that normally banks may not.Lending Club offers better rates than a bank would, and loans are issued much faster. Lending Club and Prosper charge a 5% origination fee. The origination fee you pay for your loan will depend on your loan rate. The safest borrowers with the best credit pay the lowest origination fees, while mostly everybody else pays a 5% fee. Lending Club because they get better rates than they would with a bank loan and loans are issued much faster through the power of the crowd. The crowd will also approve loans that normally banks may not.Lending Club offers better rates than a bank would, and loans are issued much faster. On average, Lending Club generally charges a 5% origination fee. The origination fee you pay for your loan will depend on your loan rate. The safest borrowers with the best credit pay the lowest origination fees.

Question Four:

Hey Guys, I just finished listening to all of the rental property episodes (I've been setting them aside for a day off so I can focus on them rather than listening to them on the six train) and I'm hooked. I know you give your feedback on the episodes, but I was wondering if you have any top of the listed advice when using Rootstock, or just rental investing in general? I do notice that the listing prices on Rootstock are slightly above what they are on a website such as Zillow/Trulia (double checked with your tool as well). What's your thought on this and is this where you would take into consideration a lower offer price? One: Always negotiate! Some sellers won't budge, but it never hurts to ask. Two: View your basket of properties as one entity. Everything balances itself out. Some properties will perform better than other but may be riskier. Others may bring in less cash flow but overall less risky. Three: Find a reliable property manager. It will make your life so much easier. Make sure they are up to date with their technology and responsive. Four: Find a great bank. Working with the same people makes it all easier and automatable. Having all your loans in place makes accounting easier.Question Five:

Hey Guys, I have been exploring the Roofstock marketplace. One thing I am having an issue with is the areas these relatively low-cost properties are located in, for example, Jacksonville, FL. I think you mentioned you purchased a property for around $50k (great deal by the way). I am going to wildly guess that it is in Florida. If I compare the school ratings of the cheaper properties on Rootstocks, the ratings are extremely low (1-2 ratings). I am looking to pull the trigger and buy a property in Rootstocks soon. I already have pre-approval for a loan. Just want to know your thoughts. Did you forego school ratings and focus just on cash flow? Any help is appreciated! There are different strokes for different folks. You need to find a strategy that works for you and the area you decided to invest in. Cash flow is super important when choosing a property. However, even if it's the best deal of the century if the crime rates and vacancy rates are high, it might be more of a headache than it's worth. On the other hand, if you find a great deal on a property with low elementary school ratings but it in a collage town where you will be renting to students, the lower school rating won't matter so much.462 episodes